Articles and News

YouGov Releases Latest Affluent Data About Jewelry, Money, Politics, and Spending | May 04, 2016 (0 comments)

New York, NY—America’s affluent are doing better than ever financially, according to the annual YouGov Affluent Perspective Global Study. But with uncertainty in overseas economies and American politics, their mood is more cautious than in recent years.

The findings of the study were presented Tuesday by Cara David, managing partner and chief study officer, and Dr. Jim Taylor, a professor at Michigan State and a consultant to YouGov.

Taylor and David surveyed 2,515 affluent American consumers and 2,743 affluent consumers globally. The total sample covered the top 10% of earners in the United States, defined as those with household income above $150,000. Of those, Taylor and David sub-divided the results among three groups: the base affluent ($150k-$199k), middle affluent ($200k-$349k) and upper affluent ($350k+).

Globally, this represents 75% of all income on the planet, said Taylor. Additionally, the income gap is real: 75% of all assets are held by the affluent community and of those, 50% are held by the wealthy community—those with incomes of $400,000 or more.

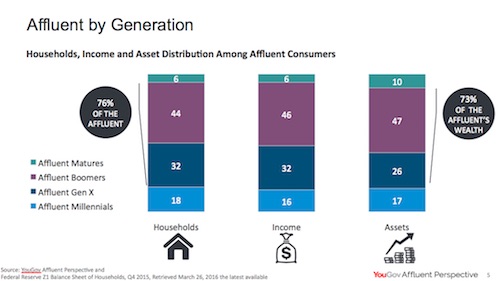

Generationally speaking, 18% households in the affluent world are Millennials, and they are wealthier at this point in their lives than their parents ever were. But 46% of all assets and income still is in hands of the Boomers, who control the lion's share of wealth in the United States, said Taylor. Gen X, meanwhile, the group of affluents sandwiched between the giant Boomer and Millennial cohorts, controls 32% of all income and 26% of all assets.

“Don’t chase the nickels and ignore the dollars!” he warned luxury marketers who are focused on Millennial consumers.

While current U.S. economic data doesn’t suggest a recession is on the horizon, the uncertainty is making affluent consumers a little nervous, said Taylor, which means their spending may be adjusted accordingly as they create a cash moat to insulate themselves in the event of any kind of downturn. The US GDP is forecast to increase 2% this year, but affluent respondents to the study say they’re going to be holding steady on spending, if not trimming just a little—a slight decline of 0.9% in discretionary spending is forecast for the affluent population.

The affluent community isn’t anticipating any financial hardships, says Taylor, but memories of 2008 die hard. Affluent Americans are very invested in bolstering their savings and making sure their personal bottom lines don’t suffer no matter what happens externally.

“On a technical basis, there’s no recession on the horizon. But on an attitude basis, there could be if the affluent community shuts its wallets,” says Taylor. These are the people who run companies, he said, and if they don’t feel confident they could actually create a self-fulfilling recession prophecy.

Not surprisingly, politics is making everybody nervous. The YouGov survey found the number-one source of anxiety among affluent and non-affluent alike is the election: it’s a source of angst for 80% of non-affluent consumers (also surveyed by YouGov) and 79% of affluent respondents to this study. And more than a third of the world also is watching warily: 36% of global affluents in the YouGov study are worried about the U.S. election.

The income gap, however, is of less concern to this cohort. While almost half (48%) of non-affluent consumers find it a concern, 39% of affluents think it’s a major issue. Most of those concerned are Millennials. But among all consumers—affluent and non-affluent alike—the overall happiness meter is pretty high. Most consumers feel their lives are good and they’re satisfied with where they are. The universal concern is what kind of a future their children will have, with issues like gun control, global warming, and potential threat from ISIS resonating.

The good news is that even if affluent households do experience a financial change, their adjustments will be to trade down, not eliminate, spending. Two categories they’re willing to cut back on are dining out and leisure travel—both categories that have rocketed in spending since the Great Recession. A variety of categories, including home décor, fashion, jewelry, and watches already has been experiencing slow to negative growth. Taylor attributes a lot of that change to some older consumers spending for experiences rather than physical goods.

But it’s not the case across the board, and one of the most important revelations to emerge from this study is how consumers enter the luxury market. The way—and time—a consumer enters the luxury market has a lifelong impact on his or her spending for luxury goods, said Taylor and David.

60% of all luxury consumers—and especially Millennials—entered the luxury market with a gift or reward or special occasion at a fairly young age. 55% said that first experience increased their interest in other luxury categories, and 62% said they still use the brand from that first experience.

A pivotal shift has occurred, according to the results of the study. The percentage of luxury consumers who had their first luxury experience by age 37 (the leading edge of the Millennial generation) was a whopping 90%. Compare that to 72% of Gen-X (age 38-51), 61% of Boomers (age 52-70), and 55% of Matures (age 71+). Boomers, and especially Matures, often were the first generations of their families to achieve luxury, self-made and later in life. But they’ve introduced their offspring to it in childhood or, at most, in teenhood. Another key difference is that while their own first experience with luxury was likely to be dining or travel, their children’s first experience is likely to have been with a product such as a handbag or piece of jewelry.

“Boomers are catalysts! Salespeople have to be trained to ask Boomer customers if the purchase is a gift for their kids—and show them stuff Millennials like!” emphasized Taylor.

David related a recent personal experience: she does a lot of shopping for her Millennial-age daughter. She bought an outfit, but later realized it wasn’t anything her daughter would wear, so she went back to the store to return it. The clerk processed the return without ever once attempting to show her something different that her daughter might like.

The Boomer catalysts are getting the younger generation addicted to luxury, explained Taylor. Despite their reported cynicism, 56% of Millennials it the study said luxury brands are worth every dime, compared to 34% of Gen-X, 23% of Boomers, and 27% of Matures.

56% of Millennials expect to spend more on luxury than last year—though Taylor did say it could end up on some off-price sites like Gilt Groupe. He also mentioned that the secondary luxury market is huge among Millennials, including auctions and other sources of second-hand goods.

Luxury is a maturation process, he said, not an end state in the process of learning to shop for beautiful things. For young people, the only thing they know is price, and they do see that as a principal discriminator for luxury vs. non luxury. 69% of Millennials see price as indicator of true luxury, but that percentage declies to 51% of Gen-X, 39% of Boomers and 37% of Matures.

“Older generations know how to look for quality in seams, buttons, furniture joints, etc.,” explains Taylor. “Salespeople have to become docents,” he said.

Experience brings understanding, he said. The longer someone is in the luxury market, the more important quality, comfort, and pleasure become. Not surprisingly, status and a perception of elegance are key motives for Millennial luxury shoppers, whereas indulgence is the key motivator for older shoppers.

“Power resonates with Millennials because it speaks for them. Luxury brands reflect a certainly level of professional achievement, and are a social currency to communicate things about people that other brands don't. That leads to self-confidence help fit into and have influence within the crowd,” says Taylor.

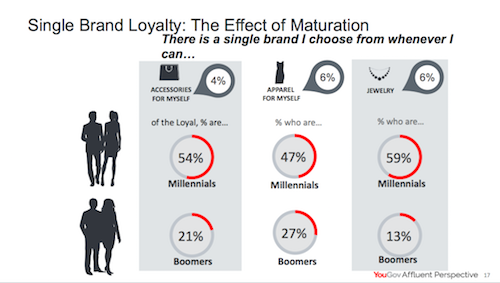

Luxury is at a crossroads in general, he said. Looiking at consumers who say "There is a single brand I choose from whenever I can," is a relatively low percentage but for jewelry it's higher among Millennials than Boomers.

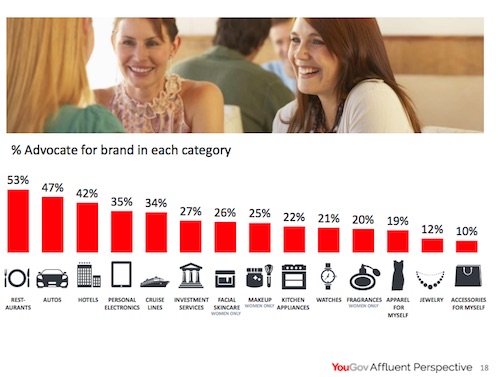

There are five stages on the road to advocacy, which is what any brand wants its consumers to achieve. First, as stated, consumers experience a gift or reward. The next step is a repeated experience. Next is loyalty to a brand (or not, if they’re disappointed by it). Next comes a self-confidence stage and last, the advocacy stage where they’re eager to share their knowledge of brands and luxury. The categories where they’re most likely to be brand advocates are restaurants, autos, hotels. Jewelry and apparel are low on that scale—but they have the biggest effect on spending. A person who is loyal and an advocate for a jewelry brand spends 69% more than non-advocate, says Taylor. Compare that to only a 17% spread in the spending of a hotel advocate vs. non-advocate.

Jewelry has one of the lower percentages of brand advocates, but those advocates spend a lot more in the category than non-advocates. By contrast, restaurant advocates, though greatest in number, only spend about 14% more when eating in their favorite dining spot than non-advocates.

“Advocates are information hogs. They read your email and promotions, they want to know what's happening to your brand and company, and they comment online and share information—and Boomers are just as active as Millennials,” said Taylor. Still, most advocacy happens in person: people who spend more on average are in your stores, he added.